Small and Medium Enterprises (SMEs) are important to the economic growth and development of Pakistan. However, SMEs often face significant challenges in accessing finance, primarily due to the lack of collateral and high delivery costs. To address these challenges, the State Bank of Pakistan (SBP) has introduced the SME Asaan Finance (SAAF) scheme, a subsidized facility with risk coverage to facilitate easier access to credit for SMEs. This scheme is designed to encourage banks to invest in human resources, technology, and processes to better serve the SME market.

Table of Contents

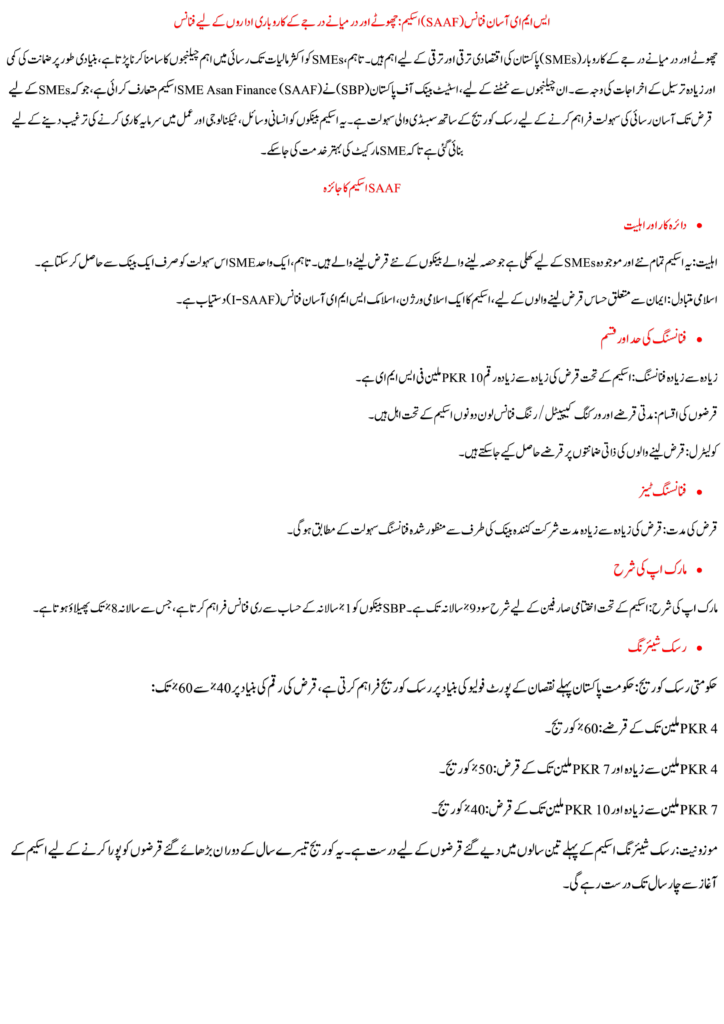

ToggleOverview of the SAAF Scheme

Key Features

Scope and Eligibility

- Eligibility: The scheme is open to all new and existing SMEs that are new borrowers of participating banks. However, a single SME can avail this facility from only one bank.

- Islamic Alternative: For faith-sensitive borrowers, an Islamic version of the scheme, the Islamic SME Asaan Finance (I-SAAF), is available.

Financing Limit and Type

- Maximum Financing: The maximum loan amount under the scheme is capped at PKR 10 million per SME.

- Types of Loans: Both term loans and working capital/running finance loans are eligible under the scheme.

- Collateral: Loans may be secured against personal guarantees of the borrowers.

Financing Tenor

- Loan Tenor: The maximum duration of the loan will be as per the financing facility approved by the participating bank.

Rate of Mark-up

- Mark-up Rate: The interest rate for end-users under the scheme is up to 9% per annum. SBP provides refinance to banks at 1% per annum, allowing a spread of up to 8% per annum.

Risk Sharing

- Government Risk Coverage: The Government of Pakistan provides risk coverage on a first-loss portfolio basis, ranging from 40% to 60% based on the loan amount:

- Loans up to PKR 4 million: 60% coverage.

- Loans exceeding PKR 4 million and up to PKR 7 million: 50% coverage.

- Loans exceeding PKR 7 million and up to PKR 10 million: 40% coverage.

- Validity: The risk sharing is valid for loans disbursed within the first three years of the scheme. The coverage will remain valid for four years from the launch of the scheme to cover loans extended during the third year.

Implementation Details

Refinancing and Risk Coverage

- Refinancing Period: SBP will provide time-bound refinancing for three years to banks selected through a transparent bidding process. After 3 years, banks will repay the refinanced amount in 10 equal divided yearly installments.

- Risk Coverage Period: The risk coverage will be valid for four years, ensuring that loans extended in the third year are suitably covered.

Guarantee and Risk Sharing

- Loan Infections: The risk sharing will align with SBP’s classification and provisioning criteria for SME financing. This ensures that the profit and loss accounts of participating banks remain unaffected as long as loan infections stay below the risk coverage levels.

- Expiry of Guarantee: The guarantee/risk sharing facility will end four years after the scheme’s initiation. The last payment under the risk sharing facility will cover infections recognized at the end of the last quarter of the fourth year.

- Portfolio Categories: The risk coverage percentages are applied separately for each portfolio category, and the residual risk coverage cannot be transferred between categories.

Participation and Selection of Banks

- Expression of Interest (EOI): SBP invites banks to express their interest in building their SME loan portfolio during the scheme’s three-year validity period. Banks offering the highest portfolio size and the largest number of borrowers will be selected for participation.

- Categories of Banks: The scheme will select a maximum of eight banks from four categories:

- Large Banks

- Mid-sized Banks

- Small Banks

- Any category of banks supported by Fintech

- Application Deadline: Banks are encouraged to apply as per the EOI to SBP within four weeks from the issuance of the circular.

How to Apply

Interested banks must submit their applications as per the guidelines provided in the Expression of Interest (EOI) document. The EOI, along with detailed information on the scheme, can be found in the following annexures:

- Annexure A-i: Scheme

- Annexure A-ii: Documents

- Annexure B-i: (1-SAAF) – Scheme

- Annexure B-ii: Islamic (1-SAAF) – Documents

- Annexure C: Expression of Interest Document

FAQs: SME Asaan Finance (SAAF) Scheme

1. What is the SME Asaan Finance (SAAF) Scheme?

The SME Asaan Finance (SAAF) Scheme is a subsidized financing program introduced by the State Bank of Pakistan (SBP) to enhance access to credit for Small and Medium Enterprises (SMEs). It aims to support SMEs by providing loans with risk coverage, encouraging banks to serve the SME market better.

2. Who is eligible to apply for the SAAF scheme?

Eligibility for the SAAF scheme includes:

- New and existing SMEs that are new borrowers of participating banks.

- Each SME can avail of this facility from only one bank.

- For faith-sensitive borrowers, an Islamic version called Islamic SME Asaan Finance (I-SAAF) is available.

3. What is the maximum financing limit under the SAAF scheme?

The maximum loan amount under the SAAF scheme is PKR 10 million per SME.

4. What types of loans are available under the SAAF scheme?

The scheme provides both term loans and working capital/running finance loans to SMEs.

5. What are the interest rates for loans under the SAAF scheme?

The interest rate for end-users is up to 9% per annum. SBP provides refinance to banks at 1% per annum, allowing a spread of up to 8% per annum.

6. What is the loan tenor under the SAAF scheme?

The loan tenor is flexible and will be determined based on the financing facility approved by the participating bank.

7. What kind of risk coverage does the SAAF scheme offer?

The Government of Pakistan provides risk coverage on a first-loss portfolio basis:

- Loans up to PKR 4 million: 60% coverage.

- Loans exceeding PKR 4 million and up to PKR 7 million: 50% coverage.

- Loans exceeding PKR 7 million and up to PKR 10 million: 40% coverage. This risk coverage is valid for loans disbursed within the first three years of the scheme and remains valid for four years from the launch of the scheme.

8. How does the refinancing and risk coverage period work?

- Refinancing Period: SBP provides refinancing for three years to selected banks. After three years, banks must repay the refinanced amount in ten equal yearly installments.

- Risk Coverage Period: The risk coverage will be valid for four years, covering loans extended during the third year.

9. How can banks participate in the SAAF scheme?

Banks must submit an Expression of Interest (EOI) to SBP within four weeks from the issuance of the circular. SBP will select a maximum of eight banks from four categories:

- Large Banks

- Mid-sized Banks

- Small Banks

- Any category of banks in collaboration with a Fintech

Conclusion

The SME Asaan Finance (SAAF) scheme is a significant initiative by the State Bank of Pakistan to enhance access to finance for SMEs. By providing subsidized loans and risk coverage, the scheme aims to address the financial challenges faced by SMEs and promote their growth and development. Banks participating in the scheme will have the opportunity to build their SME portfolios and contribute to the economic progress of Pakistan.

For more information and to apply, banks are encouraged to review the EOI and relevant annexures provided by SBP. This scheme represents a vital step towards a more inclusive financial system that supports the needs of small and medium-sized enterprises in Pakistan.